What to Do If Your Roof Insurance Claim Gets Denied

A denied roof insurance claim can be frustrating, stressful, and financially overwhelming for homeowners. After dealing with storm damage, roof leaks, hail, or wind damage, many people expect their insurance company to help cover repair or replacement costs. Unfortunately, claim denials happen more often than homeowners realize.

Insurance companies may deny roof claims for many reasons including policy exclusions, lack of maintenance, insufficient documentation, or disagreements about the cause of damage. While receiving a denial letter can feel discouraging, it does not always mean the situation is hopeless.

Understanding why roof insurance claims get denied and knowing the proper steps to take afterward can improve your chances of getting coverage approved. This complete guide explains why denials happen, what homeowners should do next, how appeals work, and how to protect yourself throughout the insurance process.

Why Roof Insurance Claims Get Denied

Insurance companies review every roof claim carefully before deciding whether to approve or deny coverage. Many denials happen because insurers believe the damage does not meet policy requirements.

Common reasons for denial include:

- roof age

- lack of maintenance

- pre existing damage

- improper installation

- excluded storm types

- insufficient evidence

- policy limitations

Understanding the reason behind the denial is the first step toward resolving the issue.

Common Reasons Roof Insurance Claims Are Denied

Every denial is different, but several issues appear frequently in roofing insurance disputes.

The Insurance Company Claims the Damage Is Normal Wear and Tear

One of the most common denial reasons is that the roof damage resulted from aging rather than sudden storm damage. Insurance policies typically cover unexpected events like hailstorms, windstorms, or falling trees. They usually do not cover natural deterioration that happens over time.

Insurance adjusters may argue the shingles were already brittle or worn before the storm occurred. If the insurer believes the roof was near the end of its lifespan, they may refuse to approve repairs or replacement. This is especially common with older asphalt shingle roofs.

Lack of Roof Maintenance

Insurance companies expect homeowners to maintain their roofing systems properly. Neglected roofs are more likely to experience preventable damage during storms.

Claims may be denied if inspectors find clogged gutters, long term leaks, mold caused by neglect, or missing shingles that existed before the storm. Regular roof maintenance records can help protect homeowners from these accusations.

The Roof Was Installed Incorrectly

Improper installation is another major reason roof claims get denied. Insurance companies may argue the roof failed because of contractor mistakes rather than storm damage.

Examples include:

- poor flashing installation

- improper nailing

- bad ventilation

- incorrect shingle placement

If the insurer believes workmanship issues caused the problem, they may refuse to provide coverage.

Damage Was Not Reported Quickly Enough

Many homeowners wait weeks or months before reporting roof damage. Insurance companies often view delays as suspicious because it becomes harder to determine the actual cause of damage.

Storm damage should be reported as soon as possible after discovery. Delayed reporting can weaken your claim and may result in denial.

Policy Exclusions

Every insurance policy contains exclusions. Some policies exclude cosmetic damage, older roofs, or certain storm related issues.

Some insurers also limit coverage for:

- wind driven rain

- cosmetic hail damage

- roofs over a certain age

Reading the policy carefully helps homeowners understand what is actually covered.

Insufficient Documentation

Insurance companies rely heavily on documentation when evaluating claims. Weak evidence can easily result in denial.

Helpful documentation includes:

- photos

- inspection reports

- weather reports

- contractor estimates

- repair invoices

The stronger your evidence, the better your chances of approval.

The Adjuster Missed Damage

Sometimes valid roof damage exists, but the insurance adjuster fails to identify it properly. Hail damage, flashing damage, and moisture problems are often overlooked during basic inspections.

This is why professional roofing inspections are so important after severe weather.

Understanding Your Insurance Policy

Many homeowners do not fully understand their roof coverage until problems occur. Insurance policies contain important details that affect claim outcomes.

Policies may include:

- replacement cost coverage

- actual cash value coverage

- exclusions

- deductibles

- depreciation rules

Understanding these terms can help homeowners avoid surprises during the claims process.

Replacement Cost vs Actual Cash Value

The type of policy you have greatly impacts how much money you may receive after storm damage.

Replacement Cost Coverage

Replacement cost coverage pays for the full cost of replacing the damaged roof minus the deductible. This type of coverage offers better financial protection for homeowners.

It usually allows homeowners to restore the roof using similar materials without major out of pocket expenses.

Actual Cash Value Coverage

Actual cash value policies factor depreciation into claim payouts. Older roofs often receive significantly reduced payments under these policies.

For example, if your roof is older and partially worn, the insurance company may only pay a portion of replacement costs.

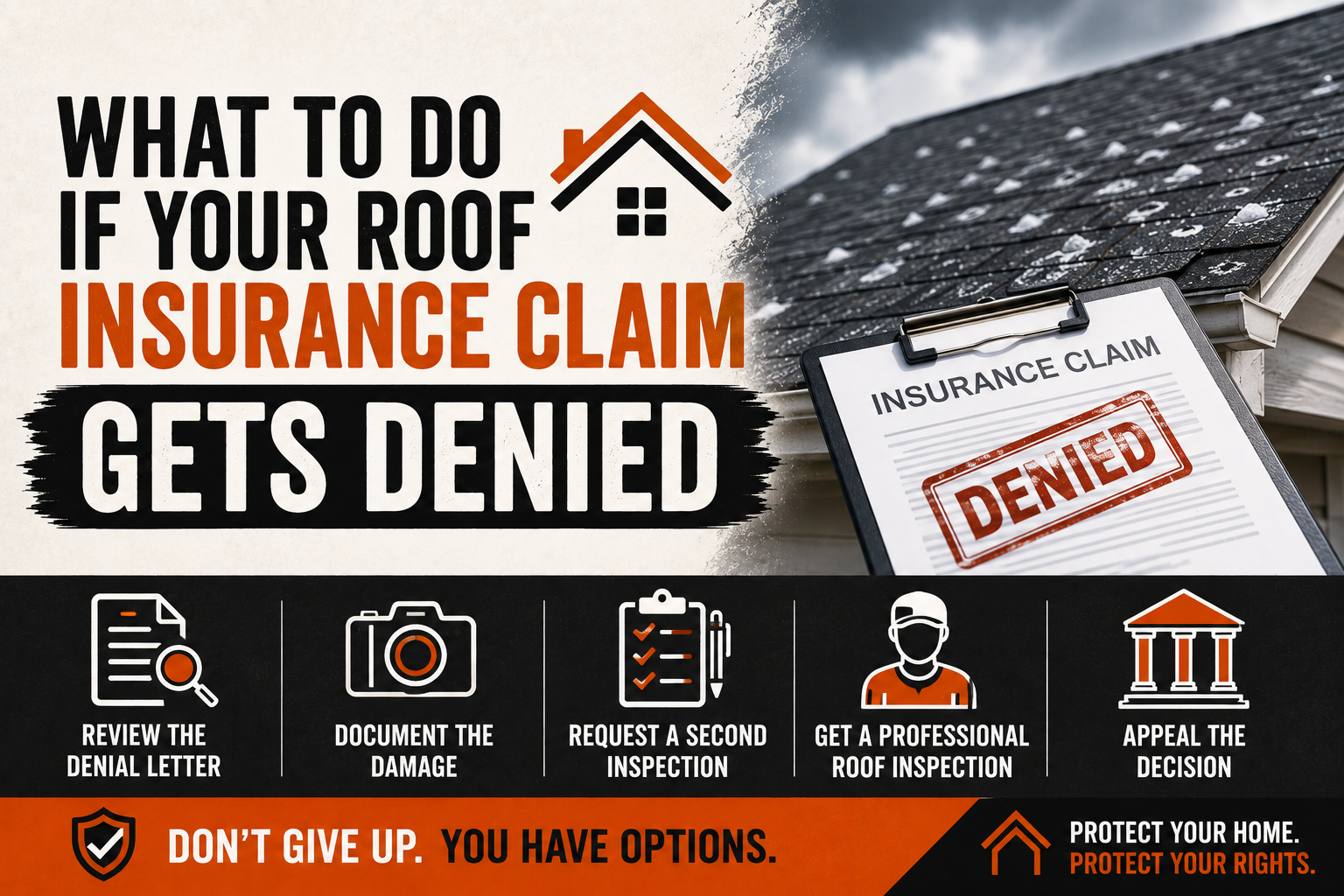

First Steps After a Roof Claim Denial

A denied claim can feel discouraging, but homeowners should remain calm and organized. Many claims are eventually approved after additional evidence or appeals.

The first step is understanding why the denial occurred.

Carefully Review the Denial Letter

Insurance companies must provide reasons for claim denials. Read the denial letter carefully and review all explanations provided.

Look for:

- policy language references

- inspection findings

- exclusions cited

- adjuster conclusions

Understanding the denial reason helps you prepare a stronger response.

Request a Copy of the Inspection Report

Homeowners have the right to request inspection documentation from the insurance company. This may include:

- adjuster notes

- photographs

- inspection summaries

Reviewing these documents can help identify errors or missing information.

Schedule-a-Professional-Roof-Inspection

Schedule a Professional Roof Inspection

Independent roofing contractors often identify damage that insurance adjusters overlook. A professional roofing inspection provides valuable evidence for appeals.

Roofing contractors can:

- document hidden damage

- identify hail bruising

- evaluate flashing

- inspect structural issues

- provide detailed estimates

Choose a licensed and insured contractor experienced with insurance claims.

Document Everything

Strong documentation is one of the most important parts of any insurance dispute. Homeowners should organize all evidence related to the roof and storm.

Helpful records include:

- before and after photos

- maintenance records

- repair invoices

- contractor reports

- weather reports

Detailed evidence strengthens your appeal significantly.

Get a Second Opinion

A second roofing opinion can reveal problems missed during the initial inspection. Different contractors may identify additional storm related damage.

This is especially useful when:

- the insurer claims no damage exists

- repairs were underestimated

- leaks continue after denial

Multiple professional assessments often improve the credibility of your case.

Understanding Roof Hail Damage Disputes

Hail damage claims are among the most disputed roof insurance claims in Texas and Oklahoma. Insurance companies sometimes argue that hail damage is only cosmetic.

However, hail can weaken shingles even without obvious leaks. Bruising, granule loss, and hidden cracking may shorten roof lifespan significantly.

Professional roofing contractors understand how to identify functional hail damage properly.

Understanding Wind Damage Disputes

Wind damage is another common source of disagreement between homeowners and insurance companies. Insurers may claim shingles were already loose before the storm.

Wind damage often includes:

- lifted shingles

- creased shingles

- exposed underlayment

- missing materials

Strong storm documentation helps support these claims.

Can You Appeal a Denied Roof Insurance Claim?

Yes. Many denied claims are later approved after homeowners submit additional evidence. Appeals are common and often successful when handled properly.

Insurance companies may reconsider claims when:

- new damage is documented

- professional reports are submitted

- errors are identified

Persistence is often necessary throughout the process.

How to Appeal a Roof Insurance Claim Denial

Appeals should be handled professionally and carefully.

Review the Policy Carefully

Study your policy language before filing an appeal. Understand:

- coverage limits

- exclusions

- deadlines

- responsibilities

Knowing the details helps you challenge incorrect denials effectively.

Write a Formal Appeal Letter

The appeal letter should include:

- claim number

- policy number

- explanation of disagreement

- supporting evidence

Remain professional and factual throughout the letter.

Submit Supporting Documentation

Attach all relevant documents including:

- inspection reports

- contractor estimates

- photographs

- weather data

- maintenance records

The more organized your evidence is, the stronger your appeal becomes.

Request a Reinspection

In many cases, homeowners can request a second inspection. Another adjuster or engineer may review the roof.

Reinspections often uncover:

- missed hail damage

- flashing issues

- moisture damage

- structural concerns

This can significantly improve claim outcomes.

What Is a Public Adjuster?

A public adjuster represents the homeowner instead of the insurance company. Their job is to evaluate damage and negotiate claims fairly.

Public adjusters may:

- inspect property

- prepare documentation

- negotiate settlements

- dispute denials

They usually work for a percentage of the final payout.

When Should You Hire a Public Adjuster?

Public adjusters may help when:

- damage is extensive

- claims are denied unfairly

- settlement offers are too low

- disputes become complicated

Homeowners should research adjusters carefully before hiring them.

Should You Hire an Attorney?

Some claim disputes eventually require legal assistance. An attorney may help if:

- bad faith practices occur

- appeals fail repeatedly

- major financial losses are involved

Legal action is usually a last resort after other solutions fail.

What Is Insurance Bad Faith?

Insurance companies are legally required to handle claims fairly. Bad faith occurs when insurers act dishonestly or unreasonably.

Examples include:

- unnecessary delays

- unfair denials

- refusal to investigate

- failure to communicate

Homeowners who suspect bad faith should document everything carefully.

Roof Maintenance Records Matter

Routine maintenance records can help homeowners defend against denial arguments. Insurance companies often ask for proof that the roof was maintained properly.

Helpful records include:

- inspection reports

- gutter cleaning receipts

- repair invoices

- contractor evaluations

These documents show responsible ownership.

Importance-of-Regular-Roof-Inspections

Importance of Regular Roof Inspections

Routine roof inspections help identify small problems before storms occur. Annual inspections also create documentation that may help during future claims.

Professional inspections can:

- identify weak shingles

- check flashing

- evaluate ventilation

- detect moisture problems

Well maintained roofs are easier to defend during insurance disputes.

Temporary Repairs After Storm Damage

Homeowners should take steps to prevent additional damage even if a claim is denied initially. Insurance policies often require homeowners to minimize further loss.

Temporary repairs may include:

- roof tarping

- sealing leaks

- replacing missing shingles

Save receipts for all emergency repairs because they may be reimbursable later.

How Roof Age Impacts Insurance Claims

Older roofs often face stricter scrutiny during insurance evaluations. Some insurers reduce coverage once roofs reach certain ages.

Older roofs may:

- receive depreciated payouts

- face limited coverage

- be excluded from replacement coverage

This is common with asphalt shingle roofs over 15 to 20 years old.

Cosmetic vs Functional Roof Damage

Insurance companies sometimes classify storm damage as cosmetic rather than functional.

Cosmetic Damage Includes:

- small dents

- discoloration

- surface blemishes

Functional Damage Includes:

- leaks

- punctures

- compromised shingles

- exposed materials

Functional damage is more likely to qualify for insurance coverage.

Questions to Ask Your Insurance Company

After a denial, homeowners should communicate clearly with their insurer.

Ask questions such as:

- What policy language supports the denial?

- Was all damage documented?

- Can a reinspection be requested?

- What evidence would change the decision?

Clear communication reduces confusion and misunderstandings.

Questions to Ask Your Roofing Contractor

Hiring the right contractor is critical during insurance disputes.

Important questions include:

- Are you licensed and insured?

- Do you handle insurance claims regularly?

- Will you document all damage?

- Can you meet with the adjuster?

Experienced contractors often improve claim success rates.

Roofing Scams After Storms

Severe storms often attract dishonest contractors. Homeowners should be cautious when approached by unfamiliar roofing companies after storms.

Warning signs include:

- pressure tactics

- demands for upfront payment

- vague contracts

- lack of insurance

Always verify contractor credentials before signing agreements.

How Long Does the Appeals Process Take?

The appeals process varies depending on:

- claim complexity

- insurance company procedures

- additional inspections

- documentation needs

Some appeals resolve quickly while others take several months.

Homeowners should remain patient throughout the process because complex claims often require multiple inspections and document reviews. Staying organized and communicating regularly with contractors and insurers can help avoid unnecessary delays.

What if the Insurance Settlement Is Too Low?

Partial approvals can still leave homeowners with large out of pocket expenses. Low settlements may not fully cover repair costs.

Homeowners may dispute low settlements by:

- submitting additional estimates

- requesting supplements

- providing contractor documentation

Supplements are common when hidden damage is discovered later.

Some insurance companies initially approve only partial roof repairs even when full replacement is necessary. Professional roofing contractors can explain why partial repairs may not solve underlying storm damage problems.

Understanding Roof Depreciation

Depreciation reduces payouts based on roof age and condition. Insurance companies calculate how much useful life the roof has remaining.

Factors include:

- roofing material

- roof age

- maintenance history

- local climate

Replacement cost policies usually offer better protection than actual cash value policies.

Texas and Oklahoma weather conditions often accelerate roof aging due to extreme heat, hail, and strong winds. Faster deterioration may reduce claim payouts if homeowners have actual cash value policies.

The Importance of Local Roofing Contractors

Local roofing contractors understand regional weather conditions and building codes. Texas and Oklahoma roofers are especially familiar with hail and wind damage.

Local contractors often:

- understand insurance trends

- recognize common storm damage

- provide faster inspections

Working with trusted local professionals is usually the safest choice.

Local contractors are also easier to contact if future warranty repairs or follow up inspections become necessary. Out of town storm chasing contractors often disappear after completing temporary work.

Preventing Future Roof Insurance Problems

Homeowners can reduce future disputes by maintaining strong records and caring for the roof properly.

Helpful steps include:

- annual inspections

- quick repairs

- proper ventilation

- gutter maintenance

- impact resistant materials

Prepared homeowners often experience smoother insurance claims.

Maintaining detailed maintenance records creates proof that the roof was properly cared for before storm damage occurred. This documentation may help challenge future denial arguments related to neglect or poor upkeep.

Best Roofing Materials for Storm Protection

Some roofing systems resist severe weather better than others.

Popular options include:

- Class 4 impact resistant shingles

- standing seam metal roofing

- synthetic roofing materials

Upgraded roofing systems may help reduce future damage and insurance disputes.

Impact resistant shingles are especially popular in storm prone areas because they are designed to handle hail impacts more effectively. Some insurance companies even provide premium discounts for homes with upgraded roofing systems.

How Severe Weather Affects Texas and Oklahoma Roofs

Texas and Oklahoma experience frequent:

- hailstorms

- tornadoes

- windstorms

- extreme heat

These conditions create high roofing insurance claim activity throughout the region.

Extreme summer heat can also weaken shingles over time. Roofing materials expand and contract constantly during temperature changes. This gradual stress may worsen storm damage during severe weather seasons.

Homeowners in these regions should schedule regular roof inspections because weather conditions are often unpredictable. Preventive maintenance can reduce the chances of severe damage and future insurance disputes.

What Happens if You Ignore Roof Damage?

Ignoring storm damage can lead to:

- worsening leaks

- mold growth

- structural weakening

- insulation damage

- higher repair costs

Unrepaired damage may also complicate future insurance claims.

Even small roof leaks can create major problems inside the home. Water intrusion often spreads into ceilings, walls, and attic spaces before homeowners notice visible warning signs.

Long term moisture exposure may weaken wood framing and roof decking. Mold growth can also develop quickly in humid attic environments. These issues become much more expensive to repair when left untreated.

Insurance companies may also deny future claims if they believe homeowners failed to prevent additional damage after the original storm event.

Roof Insurance Claim Checklist

After storm damage:

- inspect the property safely

- photograph all damage

- contact a roofing contractor

- notify your insurance company

- save receipts and documents

- review your policy carefully

- request reinspection if denied

Organization is essential throughout the process.

Homeowners should keep all claim related documents together in one location. This includes emails, inspection reports, invoices, photos, and conversations with insurance representatives.

Detailed records help avoid confusion during the claims process. Organized documentation also improves communication between homeowners, contractors, and insurance companies.

Common Mistakes Homeowners Make After Denials

Accepting the Denial Immediately

Many homeowners assume the insurance company’s first decision is final. In reality, appeals often succeed when additional evidence is provided.

Insurance adjusters sometimes miss hidden damage or underestimate repair needs. A professional roofing contractor may identify serious issues during a second inspection.

Failing to Gather Evidence

Weak documentation makes disputes harder to win. Photos and contractor reports are extremely important.

Homeowners should photograph:

- damaged shingles

- gutters

- flashing

- interior leaks

- storm debris

Clear evidence strengthens claims significantly.

Hiring Unqualified Contractors

Poor inspections weaken claims and create confusion.

Some contractors lack experience handling insurance disputes. Others may fail to document damage properly or provide vague repair estimates.

Always choose licensed and insured roofing contractors with strong local reputations and storm damage experience.

Waiting Too Long

Delays may hurt both repairs and appeal opportunities.

Insurance companies often impose claim deadlines. Waiting too long may allow damage to worsen and make it harder to prove the original storm caused the problem.

How Professional Documentation Helps

Detailed contractor reports provide stronger evidence during disputes. Professional documentation often includes:

- damage measurements

- moisture readings

- inspection photos

- repair recommendations

Well organized evidence can make a major difference during appeals.

Roofing contractors may also provide drone photography and attic inspections to document hidden problems. Advanced inspection tools often reveal moisture damage that basic inspections miss.

Comprehensive reports help homeowners challenge inaccurate adjuster conclusions more effectively.

Why Roof Ventilation Matters During Insurance Claims

Roof ventilation affects roof condition more than many homeowners realize. Poor ventilation can accelerate shingle aging and moisture buildup.

Insurance companies sometimes deny claims when they believe ventilation problems contributed to roof failure. Proper attic airflow helps prevent excessive heat and moisture damage.

Homeowners should ensure:

- attic vents remain clear

- insulation is balanced

- ventilation systems function properly

Documenting proper ventilation maintenance can help during disputes.

Poor ventilation may also cause shingles to deteriorate faster during hot summer months. Trapped heat can weaken roofing materials and shorten roof lifespan significantly.

Proper attic airflow improves energy efficiency while helping the roofing system perform better during extreme weather conditions.

How Roof Leaks Become Worse Over Time

Small roof leaks often appear harmless initially. However, even minor moisture intrusion can spread quickly throughout the home.

Over time, leaks may damage:

- insulation

- drywall

- wood framing

- ceilings

- electrical systems

The longer repairs are delayed, the more expensive the damage often becomes.

Water can travel far from the original roof leak before becoming visible inside the home. Some homeowners only discover leaks after major ceiling stains or mold growth appear.

Quick action after storms helps minimize repair costs and protects the home from larger structural problems.

Understanding Supplemental Insurance Claims

Sometimes contractors discover additional hidden damage after repairs begin. Supplemental claims allow homeowners to request additional insurance funds.

Supplements commonly involve:

- rotten decking

- hidden moisture damage

- damaged flashing

- structural repairs

These claims are common during major roof restoration projects.

Many roofing systems have hidden layers that cannot be fully inspected until shingles are removed. Contractors often uncover damaged decking or moisture trapped beneath roofing materials.

Insurance companies may approve supplemental payments when contractors provide proper documentation of newly discovered damage.

Why Insurance Adjusters and Roofers Disagree

Insurance adjusters and roofing contractors sometimes have different opinions regarding damage severity. Adjusters work for insurance companies while contractors focus on repair needs.

Disagreements often involve:

- scope of damage

- replacement necessity

- material pricing

- hidden issues

Professional documentation helps resolve these disputes more effectively.

Roofing contractors often spend more time inspecting the roof than insurance adjusters. This allows contractors to identify subtle storm damage that quick inspections may overlook.

Homeowners benefit when contractors communicate directly with adjusters during reinspections or supplemental claim reviews.

The Role of Weather Reports in Roof Claims

Weather reports can strengthen storm damage claims significantly. Insurance companies often verify whether severe weather occurred in your area.

Helpful weather documentation may include:

- hail reports

- wind speed data

- storm tracking records

- local weather alerts

This evidence supports the timing and severity of roof damage claims.

Professional roofing companies sometimes use specialized weather tracking services to confirm storm activity near the property. These reports help connect roof damage directly to specific weather events.

Detailed weather documentation can improve claim credibility during appeals.

Why Older Roofs Face More Insurance Challenges

Older roofs naturally experience wear and tear over time. Insurance companies often argue that storm damage affected already weakened materials.

This creates more disputes regarding:

- depreciation

- maintenance responsibility

- replacement necessity

Homeowners with older roofs should document maintenance carefully to strengthen future claims.

Some insurers may refuse to renew policies on aging roofs altogether. Others may require homeowners to replace old roofing systems before continuing full coverage.

Routine maintenance and inspections become especially important as roofs age.

How Roof Material Impacts Insurance Claims

Certain roofing materials perform better during storms and may influence insurance decisions.

Asphalt Shingles

Asphalt shingles are common but more vulnerable to hail and wind damage.

Metal Roofing

Metal roofs generally resist storms better and may qualify for insurance discounts.

Tile Roofs

Tile roofing is durable but can crack during severe hailstorms.

Impact Resistant Shingles

Class 4 shingles are designed to withstand stronger impacts and may reduce future claims.

Insurance companies sometimes offer lower premiums for impact resistant roofing systems. These materials reduce the likelihood of storm related losses over time.

Choosing durable roofing materials may help homeowners avoid future disputes and expensive repairs.

Preparing for Future Storm Seasons

Preventive preparation helps homeowners reduce future damage risks.

Before storm season:

- schedule roof inspections

- clean gutters

- trim tree branches

- repair loose shingles

- inspect flashing

Preparation reduces the likelihood of severe storm damage.

Homeowners should also inspect attic spaces regularly for moisture or ventilation problems. Small roofing issues often become worse during severe storms.

Taking preventive action before storm season can save thousands of dollars in future repair costs.

Signs You Should Replace the Roof Instead of Repairing It

Sometimes repairs are no longer cost effective. Insurance disputes become more common when roofs approach the end of their lifespan.

Signs replacement may be necessary include:

- repeated leaks

- widespread shingle damage

- severe storm impacts

- multiple past repairs

Professional contractors can determine whether replacement is the better investment.

Frequent repairs may eventually cost more than installing a new roofing system. Older roofs also tend to experience more storm related damage during severe weather.

A full replacement often improves long term protection, energy efficiency, and property value.

How Roof Insurance Claims Affect Home Sales

Roof condition strongly affects real estate transactions. Denied claims or unresolved roof damage may create problems when selling a home.

Potential buyers may worry about:

- future leaks

- hidden damage

- insurance difficulties

Keeping roof records organized helps reassure buyers.

Home inspections often reveal roofing problems during the sale process. Buyers may request repairs or price reductions if roof damage remains unresolved.

A well maintained roof improves buyer confidence and helps homes sell more easily.

Roof Insurance Deductibles Explained

Deductibles represent the portion homeowners pay before insurance coverage begins.

Some policies include:

- standard deductibles

- percentage based wind deductibles

- hail deductibles

Understanding deductible amounts helps homeowners prepare financially after storms.

Percentage deductibles are common in storm prone states like Texas and Oklahoma. These deductibles are often based on a percentage of the home’s insured value.

Homeowners should review deductible details carefully before filing claims.

The Importance of Keeping Communication Records

Homeowners should save all communication related to their insurance claim. Emails, phone call notes, and text messages may become important later during disputes or appeals.

Keeping records helps homeowners track:

- claim updates

- inspection schedules

- adjuster statements

- settlement discussions

Detailed communication records help avoid misunderstandings and provide proof if disagreements occur later.

It is also helpful to write down the names of insurance representatives and adjusters involved in the claim. Organized records improve accountability and help homeowners follow the progress of their case more effectively.

How Roof Claims Impact Future Insurance Premiums

Many homeowners worry that filing a roof claim will automatically increase insurance costs. While claims can sometimes affect premiums, storm related claims are often treated differently than preventable losses.

Insurance companies usually evaluate:

- claim frequency

- regional storm activity

- home condition

- roofing material quality

In storm prone states, widespread weather events often affect many homeowners at once.

Replacing an old roof with impact resistant materials may actually reduce future premiums in some situations. Homeowners should ask insurance providers about potential discounts after roof upgrades.

Why Homeowners Should Never Ignore Denial Deadlines

Insurance policies often include strict deadlines for appeals and supplemental claims. Missing these deadlines may prevent homeowners from challenging denied claims later.

Deadlines may apply to:

- submitting appeals

- requesting reinspections

- providing documents

- completing repairs

Reviewing policy timelines carefully is extremely important after receiving a denial letter.

Homeowners should respond quickly even if they are still gathering evidence. Prompt communication shows the insurance company that the homeowner is actively pursuing the claim.

Final Thoughts

A denied roof insurance claim can feel overwhelming, but homeowners still have options. Many denials happen because of incomplete documentation, missed damage, or disagreements about roof condition rather than intentional wrongdoing.

By understanding your insurance policy, gathering strong evidence, working with experienced roofing professionals, and pursuing appeals when appropriate, you can improve your chances of receiving fair coverage for storm related roof damage.

The most important thing homeowners can do is act quickly, stay organized, and remain persistent throughout the process.

Storm damage should never be ignored, and a denied claim does not always mean the end of the road. With the right approach, many homeowners successfully overturn denials and obtain the support needed to restore and protect their homes.

Leave A Comment